Statistical Arbitrage

Description

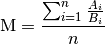

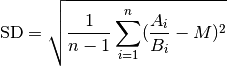

Statistical Arbitrage (SA) is build to gain profit on simultaneously buying and selling two shares of two correlated instruments. It is recomended to find two securities that are in the same sector / industry, they should have similar market capitalization and average volume traded. SA Strategy calculates two following values, which are later used to generate proper trade signals:

- Mean (M) ratio of the first

periods prices of two assets

periods prices of two assets - Standard deviation (SD) of ratio of the first periods prices of two assets

where is a Number of Periods.

Mean and standard deviation are defined as follows:

where  (

( ) is a price of the first (second) asset at the moment

) is a price of the first (second) asset at the moment  .

.

SA strategy starts decision rule, if orders should be sent after receiving Number of Periods trades.

Market Data

- Latest Tick

Parameters

| PARAMETER NAME | DESCRIPTION | ESSENTIAL |

|---|---|---|

| Number of Periods | Number of last ‘last trades’ events taken into account in a computation of the mean and standard deviation | Yes |

Conditions

Open position

Consider an arbitrary moment  , when strategy has no opened positions. If

, when strategy has no opened positions. If  then we buy asset A and sell B.

then we buy asset A and sell B.

Close position

Consider an arbitrary moment  we should close these two positions when

we should close these two positions when  .

.

Termination

There is no strategy termination condition.

Time frame

This strategy is dedicated to run in a long period of time. The instruments are highly correlated, so it is not likely that the ratio of prices will differ from mean by two standard deviations.

Further information & source

- Barry Johnson, Algorithmic Trading & DMA: An introduction to direct access trading strategies, 4Myeloma Press, 2010.