Slow Stochastic Oscillator

Description

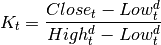

Slow Stochastic Oscillator Strategy is build to gain profit on buying / selling shares in a specific market conditions. This strategy is driven by some function (will be define later) of the following indicator which is parametrized by

where  equals Number of Periods. Moreover,

equals Number of Periods. Moreover,  is a closing price in a period

is a closing price in a period  and the value of

and the value of  is the lowest (the highest) price from the last periods.

is the lowest (the highest) price from the last periods.

On a base of a  we can compute its smoothed version:

we can compute its smoothed version:

which is smoothed again to obtain our final index:

Slow Stochastic Oscillator strategy starts decision rule, if orders should be sent after Number of Periods + 4 periods. Observe that this is the first moment in which  index can be computed.

index can be computed.

Market Data

- Last trade

Parameters

| PARAMETER NAME | DESCRIPTION | ESSENTIAL |

|---|---|---|

| Number of Periods | Number of ‘periods’ taken into account in a computation of the |

Yes |

| Oversold Level | Upper boundary of the index values area where market is oversold |

Yes |

| Overbought Level | Lower boundary of the index values area where market is overbought |

Yes |

Conditions

Open position

If strategy does not have an open position and:

algorithm opens long position

algorithm opens long position algorithm opens short position

algorithm opens short position

Close position

If strategy does have an open position and:

- algorithm close short position

algorithm close long position

algorithm close long position

Termination

There is no strategy termination condition.

Time frame

Strategy bases on some initial Number of Periods + 4 of data collection without trading and is designed to enable adjusting both: period of data collection and its trading time span from hours to whole weeks.