HFT – the good, the bad and the ugly

High Frequency Trading, known also as HFT, is a technology of market strategies execution. HFT is defined by technically simple and time costless algorithms that run on appropriate software optimized for data structures, level of memory usage and processor use, as well as suitable hardware, co-location and ultra low-latency data feeds.

Although HFT exists on the market for over 20 years, it has became one of the hottest topic during past few years. It is caused by several factors, such as May 6, 2010, “Flash crash”, latest poor situation on the market and Michael Lewis book – “Flash Boys”. Let’s look where all that fuss comes from.

The Bad

Among other things, the advantage over other market participants and ability to detect market inefficiencies is the reason why so many people critics HFT so much. Most common charges put on the table are:

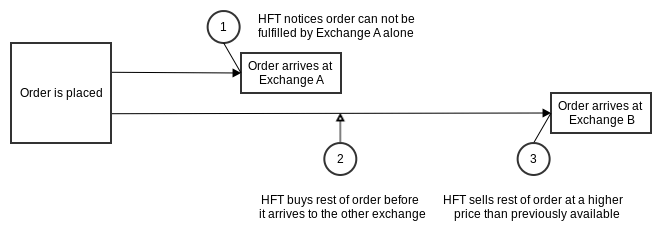

- Front Running – HFT companies use early access to incoming quotes to buy shares before other investors and then turn around and sell him just bought shares with slightly bigger price.

- Quote Stuffing – Way of market manipulation by quick sending and withdrawing large number of orders. Because of speed of operations, it creates a false impression of the situation on the market that leads other participants to executing against phantom orders. Then there is nothing else to do, but to exploit favorable prices by HFT investors.

- Spoofing – Another method for market manipulation by placing orders and then cancelling them for price increase/decrease. It is based on placing big order on the market to bait other investors, and when the market starts to react, quickly cancel it. Then new price allows to gain some profit by HFT investor.

But that’s just a tip of the iceberg. It can be often heard that there is lack of proper HFT regulations, exist false belief that there are Dark Pools without any regulations where HFT companies can hide their activity, and there is still active argument if HFT brings liquidity to the market or just useless volume.

The Ugly?

Bill Laswell once said “People are afraid of things they don’t understand. They don’t know how to relate. It threatens their security, their existence, their career, image.” That phrase perfectly fits to what is happening now on High Frequency Trading topic. When people would like to take a closer look on how exchanges work, probably, they would be less sceptic to High Frequency Trading.

Thus, on most, maybe even on all, exchanges exist two mechanism which can efficiently handle problem of quote stuffing and spoofing. First of them is limitation of number of messages per second that can be send from one client. For example on New York Stock Exchange there is a limit of 1000 messages/sec, so it means that if HFT company burst whole 1000 of messages in first half of the period, in second half it cannot send any message, so it’s cut out of the market. Other limitation used by exchanges is a limit of messages per trade. It hits even harder in quote stuffing and spoofing. In most of the cases limit is around 500 messages per trade and if someone exceed it then he should be prepared for fines. On top of it company that frequently break limits could be banned from exchange for some time.

If we talk about front running, first thing we have to know is a fact that front running, in the dictionary meaning, is illegal action, and there are big fines for caught market participants who use it. Front running is using informations about new orders before they will go to the order book. Let’s say Broker gets new order with price limit to process, but before putting it to exchange, he will buy all available shares at better price than limit and then he execute client’s new order at limit getting extra profit. That’s highly not allowed and that’s not what HFT companies do.

All they do is tracking data feed, analyzing quotes, trades, statistics and basing on that information they try to predict what is going to happen in next seconds. Of course, they have advantage due to latency on data feed and so on, because of co-location, better connection and algorithms, but it’s still fair.

(source: Wikipedia)

HFT companies have to play on the same rules as other market participants, so they don’t have any special permits letting them do things not allowed for others. Same with Dark Pools, specially that they are regularly controlled by Finance Regulators.

The Good

First, we have to know that suppliers of liquidity, i.e. Market Makers and some investors use HFT. They place orders on both sides of the book, and all the time are exposed to sudden market movement against them. The sooner such investors will be able to respond to changes in the market, the more he will be willing to place orders and will accept the narrower spreads. For market makers the greatest threat is the inability to quickly respond to the changing market situation and the fact that someone else could realize their late orders.

System performance in this case is a risk management tool. Investments in the infrastructure, both a software and hardware (including co-location), are able to improve their situation in terms of risk profile. The increase in speed is then long-term positive qualitative impact on the entire market, because it leads to narrowing of the spread between bids and offers – that is, reduce the transaction costs for other market participants, and increase of the liquidity of the instruments.

HFT AND MARKET QUALITY

In April of 2012. IIROC (Investment Industry Regulatory Organization of Canada), the Canadian regulatory body, has changed fee structure based so far only on the volume of transactions, adding the tariffs and fees that also take into account the number of sent messages (new orders, modifications and cancellations). In result, introducing new fees made trading in the high frequencies more difficult. It was very clearly illustrated by data from the Canadian market.

Directly in the following months these fees caused a decrease in the number of messages sent by market participants by 30% and hit, as you might guess, precisely the institutions that use high-frequency trading, including market makers. The consequence for the whole market was increase in the average bid-ask spread by 9%.

NO PLACE FOR MISTAKES

When people talk about HFT, both enthusiast and critics, it is not rare to hear that HFT is risk free. Well, on the face of it, after analyzing how HFT works you would possibly agree with it, but there is a dangerous side of HFT that can be not so obvious and people often forgot about it. HFT algorithms works great if the code is well written, but what would happen if someone would run wrong, badly tested or incompatible code on a real market?

We don’t have to guess it, because it happened once and it failed spectacularly, it was a “Knightmare”. Week before unfortunate 1st of August Knight Capital started to upload new version of its proprietary software to eight of their servers. However Knight’s technicians didn’t copy the new code to one of eight servers. When the market started at 9:30 AM and all 8 server was run, the horror has begun. Old incompatible code messed up with the new one and Knight Capital initiated to lose over $170,000 every second.

(source: nanex.net)

It was going for 45 minutes before someone managed to turn off the system. For this period Knight Capital lost around $460 million and became bankrupt. That was valuable lesson for all market participants that there is no place for mistakes in HFT ecosystem, because even you can gain a lot of money fast, you can lose more even faster.

SUMMARY

HFT is a natural result of the evolution of financial markets and the development of technology. Companies that invest their own money in technology in order to take advantage of market inefficiencies deserve to profit like any other market participant.

HFT is not as black as is painted.

Aldridge, Irene (2013), High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading Systems, 2nd edition, Wiley,

{kind=link}