Articles related to algorithmic trading and software tools aiding automated investment operations.

How to use Sharpe Ratio?

The Sharpe Ratio is a well-known measure of portfolio performance. It is a ratio that allows for the comparison of various portfolios and allows for the measurement of their profitability. The mathematical definition is described as a division between the expected rate of return subtracted by the risk-free rate of return and the standard deviation of rates of return [6].

In practice, the ratio is calculated annually:

The ratio describes how much excess return you are receiving for the extra volatility that you endure for holding a riskier asset ([1]). In simple words, the higher Sharpe Ratio is, the more portfolio is profitable.

Why is the Sharpe ratio so popular?

Most traders are still using the Sharpe Ratio because of its simplicity and ease of interpretation. It was proposed by Sharpe in 1966 and became credible to most users due to Nobel Prize in Economics for his works on the Capital Asset Pricing Model ([5]).

Properties of the Sharpe Ratio

With reference to [1], the ratio has several properties. It is immune to manipulation by leverage. It can be interpreted as a T-statistics to test the hypothesis (see [8]) that the return on the portfolio is equal to the risk-free rate of return. The higher ratio is consistent with a higher probability that the portfolio return will exceed the risk-free return. The investor using the ratio has a utility (see [7]) whose only arguments are expectation and variance of returns.

Forgotten assumptions

Unfortunately, most traders forget that the Sharpe Ratio doesn’t apply to every data set. The central assumption of the ratio is that the distribution of the returns is normal. The financial market should be frictionless (without financial costs), and the risk-free rate of return should be constant and identical for lending and borrowing. Also, data used for computation should contain the initial capital of the portfolio.

Consequences of the ratio

Even though it is really hard to obtain the normality of returns on every possible data, the Sharpe Ratio has other disadvantages, which are represented in [1].

The ratio does not quantify the value added, and it’s only a ranking criterion. It has a hard interpretation when the value is negative. The Sharpe ratio does not make any distinction between upside risk and downside risk.

In the case of aggregation of portfolios, the correlation between volatilities is not included in the ratio. It is suitable for investors who invest in only one fund.

It doesn’t refer to a benchmark. The choice of a risk-free rate is rather important, though the impact is weak. The result highly depends on the initial capital of the portfolio.

The sampling error of standard deviation is embedded in the values of the ratio. By using the standard deviation of returns, the Sharpe measure puts both positive and negative variations from the average on the same level. But most investors are only afraid of negative variations.

As a consequence, the Sharpe Ratio leads to inappropriate results on particular sets of data.

When the ratio fails

To be aware of how important the assumptions are, consider the following example [*]:

When the expected return is negative, the Sharpe Ratio gives the inappropriate answer. The Sharpe Ratio from Instrument A should be greater than that from Instrument B.

| INVESTMENT A | SHARPE RATIO | |||

| TOTAL RETURN | -10.00% | -1.5 | ||

| RISK-FREE RATE | 5.00% | NUMERATOR | -15.00% | |

| STANDARD DEVIATION | 10.00% | DENOMINATOR | 10.00% | |

| INVESTMENT B | SHARPE RATIO | |||

| TOTAL RETURN | -10.00% | -0.92 | ||

| RISK-FREE RATE | 5.00% | NUMERATOR | -15.00% | |

| STANDARD DEVIATION | 16.25% | DENOMINATOR | 16.25% |

The solution to Negative Returns

In the case of negative returns, the Israelsen modification of a Sharpe Ratio gives appropriate results. This ratio could be used as a verifying measure of a standard Sharpe Ratio (the values are meaningless, but the order remains accurate).

The Israelsen modification of the Sharpe Ratio from a previous example provides that Instrument A is greater than the Sharpe Ratio from Instrument B.

| INVESTMENT A | SHARPE RATIO ISRAELSEN | |||

| TOTAL RETURN | -10.00% | -0.015 | ||

| RISK-FREE RATE | 5.00% | NUMERATOR | -15.00% | |

| STANDARD DEVIATION | 10.00% | DENOMINATOR | 10.00% | |

| INVESTMENT B | SHARPE RATIO ISRAELSEN | |||

| TOTAL RETURN | -10.00% | -0.024 | ||

| RISK-FREE RATE | 5.00% | NUMERATOR | -15.00% | |

| STANDARD DEVIATION | 16.25% | DENOMINATOR | 16.25% |

In conclusion, when negative returns occur, the investor should also check the value of the Israelsen modification before making the decision.

Avoiding invalid distribution

The most dangerous ratio usage is when the distribution of the returns isn’t normal. It seems that the best idea is to check the normality of the returns before use of the Sharpe Ratio. Several statistical tests can validate data distribution, such as Shapiro Wilk, Anderson Darling, Cramer von Misses, Dagostino Pearson, Jarque Berra, Kolmogorov Smirnov, Kolmogorov Lilliefors, Shapiro Francia (see [9]).

Generalizing Sharpe Ratio

On the other hand, there are different extensions of the Sharpe Ratio, which gives more accurate results by extending different assumptions. There are plenty of them described in [1], but only those with skewness and kurtosis will be presented.

Skewness describes the asymmetry of the probability distribution. If there are more extreme returns extending to the right tail of a distribution, it is said to be positively skewed, and if they are more returns extending to the left, it is said to be negatively skewed [2].

Kurtosis provides additional information about the shape of a return distribution. Formally it measures the weight of returns in the tails of the distribution relative to standard deviation but is more often associated with a measure of flatness or peakedness of the return distribution [2].

Skewness and Kurtosis are normalized forms of 3rd and 4th central moments, respectively (see [10]). Its combination with the Sharpe Ratio allows for approximating the ratio when the distribution is not normal. This method leads to the proposition from [4], where skewness divided by kurtosis is added to the Sharpe Ratio, which results in a new performance measure.

In the case when the owner of the portfolio has different preferences (different utility – see [7]), there are other ratios to measure the performance. The Adjusted for Skewness Sharpe Ratio allows measuring the performance using hyperbolic absolute risk aversion (HARA), constant relative risk aversion (CARA), or constant absolute risk aversion (CRRA). More details can be found in [3].

Conclusion

The Sharpe Ratio is a standard measure of portfolio performance. Due to its simplicity and ease of interpretation, it is one of the most popular indexes. Unfortunately, most users forget the assumptions and that results in an inappropriate outcome. They should consider checking the distribution of the returns or validating the results with other performance measures before making a decision on the market.

References

[1] Cogneau P., Hübner G., The 101 ways to measure portfolio performance, Université de Liège

[2] Bacon C., How Sharp is The Sharpe Ratio? – Risk-Adjusted Performance Measures, StatPro Group

[3] Zakamouline V., Koekebakker S., Portfolio Performance Evaluation with Generalized

Sharpe Ratios: Beyond the Mean and Variance, University of Agder, 2008

[4] Watanabe Y., Is Sharpe Ratio Still Effective?, Journal of Performance Measurement, 2006

[*] The original example is taken from the site:

[5] http://www.investopedia.com/articles/07/sharpe_ratio.asp

[6] https://en.wikipedia.org/wiki/Sharpe_ratio

[7] https://en.wikipedia.org/wiki/Utility

[8] https://en.wikipedia.org/wiki/Statistical_hypothesis_testing

[9] https://en.wikipedia.org/wiki/Normality_test

[10] https://en.wikipedia.org/wiki/Central_moment

Crypto Signals

From Crypto Signals to Profitability: the Path of a Crypto Investor.

How do you move from earning scraps off the crypto market to profitability? Like most crypto investors, you’ve had to or are probably still pursuing different paths to profitability. You’ve often asked yourself what it takes to succeed as a cryptocurrency investor. You’ve researched the different trade strategies, explored technical analyses, tried social trading, and even went after crypto signal providers. But none of these have what it takes to turn you into a profitable crypto investor.

In this guide, we detail the average crypto trader’s journey to profitability. We take you through the different stages most investors have to go through before they can eventually turn profitable. Almost always, it starts with manual trading crypto signals and social trading for crypto trading newbies before turning to automated systems. We explore this crypto evolution, detailing the different stages at which most crypto investors are currently stuck in before letting you in on the ultimate crypto investment strategy.

Crypto Evolution

An investor’s crypto evolution is the journey they have taken in pursuit of profitability. It’s more of a learning curve with a common starting point where most crypto traders begin their investment journey. In most instances, traders start by interacting with such manual trading strategies as crypto signals. Others opt for the fully-automated crypto trading bots that are synonymous with the promise of massive returns.

Soon, they will shift to the more flexible DIY crypto trading bots that allow them to tweak the trade settings. But all these have serious faults that either cause traders to lose their investments or not make any tangible returns at all. This dims their ability to progress to pro investors. Let’s look at the stages of crypto evolution before looking at the ultimate crypto investor tool.

Crypto Signals

Crypto signals are some of the most popular crypto trading strategies for beginners. This involves linking up with a crypto signal provider, receiving trade signals, and entering into the guided positions. Different crypto signal providers, however, adopt varied tactics in their approach of the trade, with significant differences in, for example, the number of currencies they monitor, the mode of signal distribution, and signal fees. Let’s look at this in more detail:

Who Is a Signal Distributor?

Anyone with basic knowledge on how to interpret crypto charts can set up a crypto signal distribution service. A crypto signal provider is an individual or company that sends out crypto trading ideas and suggestions that its subscribers/followers can use to enter into trades. In most cases, these providers will claim to be crypto professionals or highly experienced traders. They will claim to have mastered the trade and are now just looking to help others, especially newbies, turn a coin trading the highly competitive crypto markets.

Crypto signal providers believe and have their followers believe that one can understand the markets by merely looking at the charts. They hold the opinion that they can understand the future of the markets by simply looking at its past operations. But they are wrong. And this line of thinking stems from the inherent human inclination to believe that we can draw patterns from even the most random data.

A signal service provider can also be a cryptanalysis algorithm programmed to identify the best trade entry points. When these points are triggered, the system sends out automated crypto trading signals to its subscribers.

Three types of providers, mainly the professionals that analyze the markets manually, algorithmic systems and a hybrid of algorithm and professionals traders dominate the crypto signal market. The professionals will send out signals based on the results of their market and chart analysis.

Automated traders, on the other hand, have automated systems that send out trade signals as soon as their preset trade entry triggers are hit. The hybrid signals providers, however, use the algorithms to analyze the market and identify trade entry points. But the automated trader’s results have to be counterchecked by a professional before being released to subscribers. They nevertheless have one thing in common; they all base their analysis on the results of a combination of technical analysis tools, latest news, rumors, and market conditions.

The Signal

The trade signal comprises of three critical parts: the trade entry price, the take profit price, and the stop-loss price. Depending on whether you’re dealing with free signals or paid signals, the provider will advise you on the minimum trade amounts for breaking even and maximum profitability.

Some trade signal providers may also offer additional information such as analysis of the different trade prices like the entry price or stop-loss levels. But given the time-sensitive nature of these signals, the provider will only send out the trade entry points first and the information supporting these trade points much later. You, therefore, need to fully trust that the cryptocurrency signal provider has your interests at heart given that you will enter into virtually all crypto trades blindly.

Who Uses Crypto Signals?

Crypto signals are primarily used by crypto investment beginners that can’t yet skillfully analyze the crypto markets and accurately identify the best entry and exit points. Part-time crypto investors who don’t have enough time to properly analyze crypto markets and identify the trade entry or exit points have also mostly relied on crypto trade signal providers.

Depending on signal providers to help you get into trades, however, calls for a lot of trust on the part of traders. This means you need to properly vet the signal providers before subscribing to their services. You need to look at factors such as the experience and professionalism of the individuals behind the service.

You also need to look at their win-to-loss ratio and only subscribe to the provider with the highest win ratio. Additionally, you need to consider the frequency of their trades, their subscription fees, and minimum trade amounts as well as the mode through which they distribute these trading signals.

Modes of Signal Distribution:

There is a very short window of time between receiving the signal and entering into a trade. The speed at which you enter into a winning signal ultimately determines how much you make from the trade. As such, signal providers try to use efficient modes of communication in delivering these signals to as many of their subscribers as possible. Some of the most common modes of signal distribution include:

Texts: Text message is one of the most effective and most popular method of delivering the best crypto signals. The fact that virtually everyone has a phone makes it the perfect signal distribution tool. The text message alert is also hard to ignore.

Telegram bots: Telegram messaging comes in as yet another favorite for most signal distributors. It’s easy to see why it’s the most preferred communication tool. To begin with, it has an alert system similar to that of the text message that’s hard to ignore. Secondly, Telegram allows for the development of automated trading bots that are easy to integrate into the trading systems. These will automatically enter into a trade immediately the signal is received using preset trade parameters.

Emails: Emails also count as a form of signal distribution. However, most signal providers only have them as an alternative distribution option for the text or telegram messages. Sending signals via email isn’t popular and will only work for international clients.

But latency of these channels puts investors at a huge disadvantage in comparison to for example trading bots.

Charges and other fees

A cryptocurrency signal distribution channel can be either free or paid. INFOCRYPTO and Fat Pig Signals are two of the most popular and considerably accurate free signal service providers. These two are telegram based, meaning that most of their signals are delivered via telegram bots. There’s also a host of popular paid cryptocurrency trade signal providers that charge a monthly, quarterly or annual subscription.

Why you shouldn’t consider trading signals as a crypto investing strategy:

- Virtually anyone can open an online crypto signal distribution service and charge a subscription fee. This tells you that signals providers are out to make money – not by trading but from selling untested signals. Furthermore, if these signals were as profitable as they claim, they would open trades, not sell them.

- Most virtual signal providers indicate a disclaimer that their signals are just suggestions, hence no guarantee you will profit from their execution.

- You are obliged to pay the subscription fee whether you win, lose, or fail to trade all their trade suggestions. Most will also prefer upfront payment that compounds the loss incurred from trading fake signals.

- Most will either demand for minimum trade amounts or have their subscriber fees so high that you have to commit significant trade amounts if you wish to break even

- Latency in manually entering the trade may make the signal invalid or at best diminish potential profits

Social Trading Cryptocurrency

Social trading is one of the easiest approaches to investment. It works best for both new part-time traders and investors. To successfully invest in cryptocurrencies, you need a thorough understanding and experience in analyzing the markets. You also have to stay on top of recent news and events around the crypto industry. And lastly, you have to be adept enough to predict the impact of current trends on the price of digital currencies. Social trading and the different social trade platforms that actively promote and allow copy trading can enable you to bypass the need for industry experience.

How does social trading work?

Social trading is a form of networking in crypto trading that involves sharing trade ideas and signals. The most popular form of social trading today is copy trading. Copy-trading allows a trader to copy the trade strategies of another more experienced trader. Interestingly, social trading can be implemented at both the trader expert levels exchange and trading platform level. eToro, ZuluTrade, and NagaTrader are some of the crypto trading platforms that lead the pack in supporting copy trading.

Usually, such providers will have a list of expert traders on their platform that allows others to copy their trades. Highlighted on their profiles will be such factors as their win ratio, trading frequency, coins invested in, risk tolerance levels, and historical trade accuracy. The platform will then charge either a subscriber fee or a commission on earned profits. For instance, eToro charges copy traders 20% of profits made from copying trades.

Like crypto signals, copy trading ensures you don’t need crypto trading experience to invest in cryptocurrencies. You only need a platform that lets you copy trade while maintaining the lowest social trading fees and commissions. You also need to master the art of identifying the most viable expert trader to copy from, paying particular attention to their win ratios and risk tolerance levels.

Why social trading is not the best approach to crypto investing:

- There is no guarantee that the expert trader you are copying will continue with their winning streak or good performance

- You will not always find an expert trader you are compatible with, especially when it comes to risk ratio

- Some platforms charge exorbitant fees and commissions that negatively influence your results in the long run

- Fee structures can push expert traders on the platform to risk-seeking trades thus wiping out trader accounts if the markets don’t go their way

- Social trading doesn’t create enough room for investment portfolio diversification, which additionally puts large risks on investors

BlackBox Crypto Bots

The internet and the cryptocurrency trading space isn’t short of BlackBox crypto trading bots. These are tools that claim to automate the entire crypto trading process and help you scoop unprecedented profitability, while all you have to do is buy the bot or subscribe to their service. According to their vendors, you don’t need to be a professional or highly experienced crypto trader to profit from crypto trading as these pieces of software have the work cut out for you.

The bots and software are fully automated and require little to no effort on the trader’s part. They also have efficiency, speed, and accuracy as their biggest selling points as their vendors boast of their ability to outsmart an average trader both in trade analysis and execution speeds. But even with these seemingly elite features, they have serious faults that make them unfit as a crypto investment tool.

How Crypto Bots Work

Ideally, a crypto bot is an automated trading software that crawls the cryptocurrency market looking for the best trading opportunities. Crypto bots usually follow a specific set of trade instructions when analyzing the market and identifying the best trade opportunities. These instructions are based on factors such as technical indicators, trends or price levels.

With most of the black box crypto trading bots, the settings are designed and updated by the developers of the automated trader. They leave little to no room for customization. Most are online-based as this makes it easy for developers to tweak or overhaul the trade settings more conveniently. However, when dealing with offline trading bots, the provider will send you a link where you can download new or updated trade settings and manually load them on to the bot.

Most of these bots have also embraced different levels of specialization and most crypto bots available in the market today are either coin specific or exchange specific.

Coin specific bots

These are crypto bots that are centered on the performance of a single coin. The most popular is the bitcoin bots that track and monitor bitcoin activities. Their trade settings are centered on the legacy cryptocurrency and can, therefore, only be used to trade bitcoin and bitcoin cash. They are referred to as black-box bots because there is little you can do to tweak their trade settings and their logic is generally hidden from your eyes.

Exchange specific bots

These are crypto bots developed and distributed for one crypto exchanges and its API. The bots are developed by independent crypto analysts and traders but still center on the operations of a specific exchange. Exchange specific bots will only trade some or all the coins listed on the exchange. Note also that most of the exchange specific bots often align themselves with some of the most popular exchanges like Binance, Coinbase or Gemini. They are especially popular with crypto exchanges that support leveraged crypto trades like BitMex, Kraken, and Deribit.

Who can use the bots?

Inexperienced traders: Most of these black box crypto trading bots are marketed as the ultimate hands-free and wholly passive approach to trading. And this appeals most to inexperienced crypto traders looking for a quick way to make money off the crypto market. The automated crypto trading tool especially comes in handy in allowing the inexperienced crypto enthusiast to scrap small profits from the market as they learn how to trade.

Part-time traders: Part-time crypto trading isn’t the best approach to crypto investing. The crypto market is highly volatile and leaving trades open for long – with insufficient risk management protocols in place – can expose a part-time trader to unimaginable losses in case of unexpected market downturns. Trading part-time also means that you have less time to effectively analyze the markets and set up informed trades. For this reason, most of the part-time traders have, therefore, turned to automated crypto trading bots. Their ability to use preset trade settings and incorporation of sufficient risk management tools ensures that they only enter trades when conditions are ideal.

Why crypto bots aren’t the best approach to crypto investing:

- Crypto bots are highly complicated software and arriving at a quality bot involves a lot of trial-and-error and loss of valuable capital.

- There is a lot of secrecy surrounding these automated crypto trading bots. Hardly will you ever know their developers are and this makes it hard to trust a system with your cash when you don’t know the professionalism or ethics of its developers.

- Most crypto trading bots are cloud-based and will automatically receive and execute trade signals or trade settings. They claim to use technical analysis to identify trade opportunities but will never reveal some of the indicators or trade strategies that they use.

- Fraudsters and privacy compromisers have continually targeted and infiltrated the automated crypto trading niche. Also, we still don’t have a proven method of vetting the quality of bots, the experience of their developers, the effectiveness of their strategy, and how they handle private data.

- Some automated crypto trading bots have proven time and again to be a scam only interested in your subscription fees and private data like exchange keys, and vanishing as soon as they have both. You will end up with not only your privacy compromised, but also lose both the bot subscription fee and the crypto trading capital you had invested.

- No opportunity to learn: Since everything is automated, plus the bot doesn’t share the trading strategies and technical analysis indicators used to arrive at the trades, you never get to learn how to trade.

DIY Crypto Trading Bots:

After trying crypto signals and facing the disappointment that is black box crypto trading bots, the crypto investor’s evolution journey pushes them to the DIY crypto trading bot. These DIY trading bots are automated cryptocurrency trading tools. Unlike the black box auto trading tools, however, the DIY auto traders are more professional and more transparent about their system designs and trading strategies.

They also claim to rely on technical analysis and elaborate trade strategies to analyze the market. Their DIY nature also sets them apart from the wholly automated black box auto traders that do not leave room for the customization of trade strategies. With crypto trading bots, you can tweak the default trade settings to align with factors like your risk tolerance.

Their highly transparent nature also makes it easier for you to better understand how the crypto market works. For instance, you can tell the strategy used by your DIY trading bot which technical analysis indicators should be used in monitoring the market. You can also vet its trade entry and exit decisions by setting the factors the bot takes into account before opening a trade position, risk management protocols observed for each trade, and factors triggering a sell-out and exit.

These are all part of learning that help you become a better crypto trader. In essence, the DIY bots address the inherent limitations of relying on crypto signals and the black box crypto trading bots in kick-starting your crypto journey. Two of the most popular DIY crypto trading bots in the market are CryptoHopper and 3Commas. Let’s take look at each of these below:

How Cryptohopper Works:

Cryptohopper is a Ruud Feltkamp’s project that’s currently available to crypto traders in both automated and semi-automated versions. The bot uses market and exchange arbitrage to make profits. The Cryptohopper app is also a strategy design tool that allows the user to customize trading strategies.

Cryptohopper uses technical analysis indicators such as RSI, EMA and Parabolic Sar to scan the markets. Its semi-automatic version is more of a social trading tool that copies the trade strategies of the most successful day traders and sends them out to the rest of the community.

The semi-trading bots scour the market for the best performing trade strategies, copy them, and present them to the trader. It sources trade signals from different traders and forwards them to the trader. The bot essentially presents the trader with a choice and they get to only implement the signals that they feel best matches with their trading strategy.

How 3Commas works:

3Commas describes itself as a smart trading terminal and a combination of trading bots. It features both auto-trading and manual trading systems and uses technical analyses to monitor the charts and markets around the clock. Some of the technical indicators used on the platform include CQS scalping and RSI. Plus it also supports social networking and copy-trading.

Limitations of the DIY crypto bots as professional investment tools:

While the qualities and trading features of the DIY crypto bots dwarf the crypto signals and black-box crypto bots, they are still a far cry from helping traders reap maximally from the crypto market.

- They are based on the idea that finding the right combination of simple technical analysis indicators can bring profits. Maybe it could, but this needs very good backtesting capabilities with large datasets of historical data, which all of these platforms lack.

- With current states of computing, finance, and mathematics, there are more advanced tools available than moving averages or other technical indicators capable of identifying patterns on the market

- These platforms lack the technical performance needed to react to market events. A latency of a minute or seconds outperforms signals or social trading, but is not enough to win the algorithmic race. On the contrary – you are an easy target for more sophisticated algorithms.

- Most DIY crypto trading bots have highly complicated set up processes and getting it wrong at this stage sets you up for losses every time you enter a trade

- Dealing with the bot signals and their different trade settings like where to place the stop loss and take profit levels can be quite confusing

- Most DIY bots are premium service providers that charge subscription fees. Mostly, the profits you make off your returns and time spent configuring trade settings aren’t always commensurate with the subscription fees. They have a high expense to income ratio which makes them unideal trade platforms

- Most of the DIY cryptocurrency trading tools pay more attention to social trading than educating the subscriber on how to improve their trading skills

- Most of the bots are poorly maintained and thus prone to system lags that in turn result in expensive slippages.

Ultimate Crypto Investment Tool: Professional Trading Bots

After looking at the different stages in a crypto trader’s evolution journey towards profitability and why they don’t work, you must now start revaluating your trading style. And looking at some of the reasons why it doesn’t work, you can tell that there is little you can do to turn these trading strategies around. In such a case, what are your options? Who do you turn to, especially if you are looking to undertake significant crypto investments? Well, you can always turn to professional trading bots used by expert traders and institutions.

How Do Professional Trading Bots Work?

These too are automated cryptocurrency trading systems and work to achieve pretty much the same goal as the DIY and black box crypto trading bots. However, they differ from the rest of the automated trading bots in profitability. Unlike the crypto signals and the rest of the automated tools provided by faceless individuals and companies with questionable crypto trading experience, professional bots are designed and tested by pioneer crypto traders and some of the most experienced crypto and money market trading professionals.

You will nonetheless appreciate the fact that most of these bots and platforms are proprietary and expensive. The high price is in appreciation of the time and effort as well as the resources utilized to come up with such a bot and underlying a platform that can react to market events in milliseconds, processing information on hundreds of instruments in real-time. In most instances, these bots often take months or years of hard work from highly qualified teams of professional quants and crypto traders.

Who Uses Professional Trading Bots?

Professional traders

Developing sophisticated and profitable systems requires huge time and capital investments. You need enough money to hire quants to create, test, and roll out these algorithms.

Hedge funds

Hedge funds are the primary inventors and beneficiaries of these professional crypto trading bots. They have funded the development of and own more proprietary algorithms than any other entity. And they present you with the best chance of having the professionally developed crypto bot work for you. Most don’t discriminate and will welcome any client on board as long as you can raise their minimum initial deposit.

Institutional investors

Institutional investors like mutual funds and private equity funds may also come together to fund the development of proprietary cryptocurrency algorithms.

What makes professional trading bots superior to all other approaches to crypto investing?

Here are the unique factors that make professional trading bots better than the conventional DIY and BlackBox auto traders, as well as reasons why you too should consider using one.

- Execution strategies: Virtually all professional trading bots use a combination of different trade execution strategies. And they are all aimed at helping the bot achieve maximum profitability with every executed order. The most common include:

- Smart order routing: Professional cryptocurrency bots aren’t crypto or exchange specific, but are specially designed to monitor the entire industry for the best prices. The algorithm is constantly scouring the markets looking for an exchange with the most promising prices for your orders and executing trades automatically.

- Advanced order types: A professional crypto trading algorithm also uses advanced order types not available to the retail auto traders. These include the iceberg order that hides the real size and value of your orders to ensure the market doesn’t go against you. Alternatively, it could employ the pegged order system where the algotrader passively follows the highest list of trades in the order book in a bid to achieve the best execution prices.

- TWAP and VWAP strategies – are execution algorithms that help you make large trades without influencing the prices

- Passive strategies: The bot will have liquidity provision strategies like market-making. These involve hedging and exposing your capital to minimal risk while benefiting from differences in spreads.

III. Arbitrage strategies: Arbitrage involves buying one cryptocurrency on one exchange and selling it on the other to take advantage of the price differences. It can either be standard arbitrage that involves just one cryptocoin like Bitcoin or Ethereum, or triangular arbitrage for more advanced bots that take advantage of the price difference of up to three coins in different exchanges. Other arbitrages will go as far as specializing in statistical arbitrage and cross-trading a portfolio of crypto assets simultaneously in different exchanges.

- User-defined strategies: Some bots will also have a host of advanced and statistics-based execution strategies that capture and process the widest range of data in the shortest periods to provide the trader with multiple possible correlations that can be exploited to create maximum profitability opportunities.

- Connect to both multi-list and niche exchanges: Bots for long running of stable strategies need to have regularly updated connectors to all the major crypto exchanges like Binance and Coinbase. It should also have connectors to the not-so-popular niche exchanges and over-the-counter crypto platforms. More important than the long list of connected crypto exchanges is the quality of these connectors. Exchanges are constantly changing their APIs and a professional firm who monitors and updates its connectors fast can defend you from losses that would arise from connectivity issues.

- Managed and updated by professionals: Unlike the basic crypto algorithms from faceless providers, the developers of different professional algorithmic traders are industry leaders. They are charged with the day to day management of the system by keeping it and your invested capital safe, updating its core features regularly and ensuring that it maintains optimal performance.

How do you access the professional trading bots?

We already mentioned that these professional bots have for the longest time been a preserve for the capital and digital asset management firms like hedge funds and investment banks. They are proprietary property and the tools behind the success and consistent profitability posted by these firms. Traditionally, you would have to first research the different hedge funds, looking at what they say about the features of their bots before raising a high minimum initial deposit to become one of their clients.

The recent past has however experienced a gradual change in the finance and investment industry with most institutions moving away from the traditional and rather rigid modes of business. And with this industry shift, most of these professional bots have been availed to the retail market at affordable terms for the average investor. Therefore, you no longer have a reason to continue clinging on to the frail crypto signals, the deceitful black box auto traders, the faceless ‘expert’ developers or the expensive and unprofitable DIY cryptocurrency trading bots. Learn how to access the professional proven and tested professional trading both here and start recording hedge-fund-like profits.

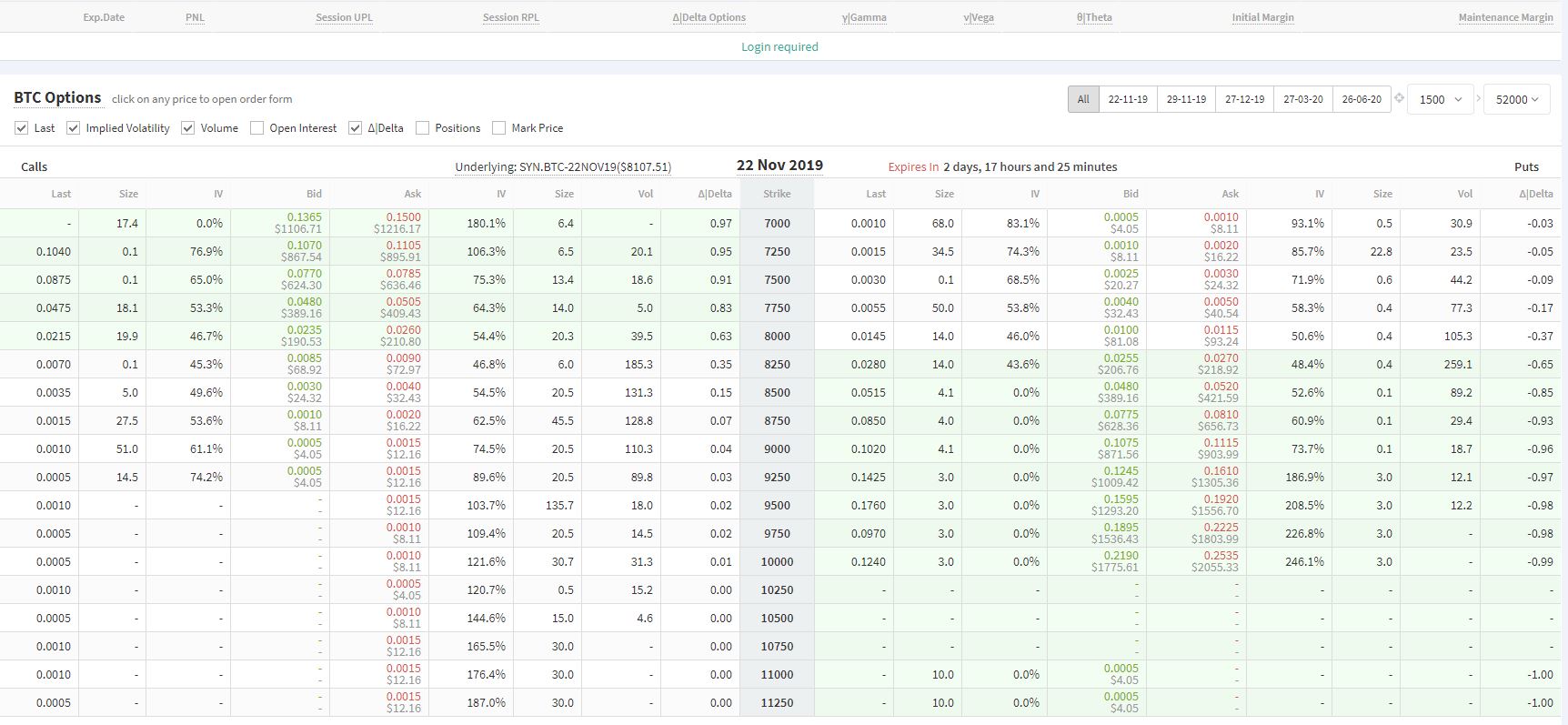

Deribit trading bot

Deribit Trading bot

Introducing Deribit Cryptocurrency Exchange:

Deribit is a cryptocurrency derivatives exchange allows for Ethereum and Bitcoin trading on Options, Perpetual and futures trading. Deribit keeps its customers’ deposits in their cold storage with most of the funds stored in vaults with multiple banks safes. Though at this point in time, Deribit only accepts Bitcoin and no fiat currency as funds to deposit. Deribit allows fully automated trading through its API.

Deribit Futures:

For futures trading on Deribit, traders receive a cash settlement instead of physical Bitcoin trading, that means the buyer of the futures do not buy the actual Bitcoin and the seller won’t sell the actual Bitcoin and what will be transferred is the transfer of profits and losses at the agreed settlement price of the contract on the expiration price.

The minimum tick size to trade futures is 0.50 USD and all daily settlements happen at the coordinated universal time (UTC) 8 am. The expiration time is also at UTC 8 am at the end of each month. The size for the contracts at Deribit future exchange is 10 USD with initial margin starting at 1.0% with a linear increment of 0.5% per 100 BTC. The delivery price is the Time Weighted Average of Deribit Bitcoin index measured in the half an hour before the UTC 8 am (7:30 am).

Deribit Perpetual

At Deribit exchange, Perpetual is a derivative very similar to Futures trading but with no fixed maturity and no exercise limit. The perpetual derivatives are to keep their price close to their underlying cryptocurrency price, which at Deribit exchange is referred to as “Deribit BTC Index”.

The Deribit Perpetual contract is 1 USD per Index Point with a contract size of 10 USD. The minimum tick size 0.50 USD and settlements are done at UTC 8 am. The contract size for trading Prepetuals in Deribit is 10 USD. As mentioned earlier there is no delivery/expiration when trading Prepetuals on Deribit.

Deribit Options:

Options on Deribit are traded with what so-called the “European style”. This indicates that options cannot be exercised before expiration, but can only be exercised at expiration. Which this happens automatically on Deribit. Options on Deribit are priced in Bitcoin and Ethereum and also viewable on USD.

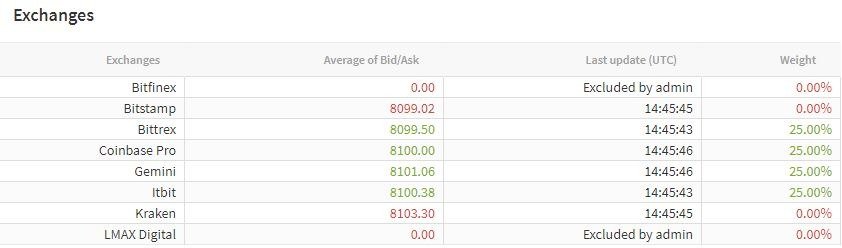

Deribit Index:

There are 8 exchanges and the highest and lowest prices are taken out, and the remaining 6 are each at 16.67% accountable for creating an index in Deribit.

Market Making on Deribit:

Deribit does not include an in-house trading desk, therefore all active market makers are the third party Market Makers. The liquidity is provided by these parties and Deribit sees these services as a crucial point to their business. Based on the volume, designated market makers receive tailored agreement on fees.

Deribit API:

For automated trading software and trading bots, Deribit provides three forms of integrating to its API, the FIX (financial information eXchange) API, JSON-RPC over Websockets API and JSON-RPC over HTTP.

Deribit utilizes JSON-RPC which is a light-weight remote procedure call protocol. The JSON-RPC specification defines the data structures that are used for the messages that are exchanged between the client software and the server, as well as the rules around their processing.

JSON-RPC is transport agnostic, it doesn’t specify which transport mechanism must be used. The Deribit API supports both Websocket (preferred) and HTTP (with limitations: subscriptions are not supported over HTTP).

Websocket is the prefered transport mechanism for the JSON-RPC API, because it is faster and because it can support subscriptions and cancel on disconnect. The code examples that can be found next to each of the methods show how WebSockets can be used from Python or Javascript/node.js.

Deribit API has public and private methods. The public methods do not require authentication. The private methods use OAuth 2.0 authentication. This means that a valid OAuth access token must be included in the request

Deribit FIX API is a subset of FIX version 4.4, but also includes some tags from 5.0 version and several custom tags. Deribit uses the standard header and trailer structure for all messages.

Trading bots:

Empirica’s trading platform has been integrated our trading bots with Deribit API in order to operate Bitcoin trading, so that our customers can use it out of the box. Let’s name some trading bots that can be applied using our trading platform through API integration on Deribit:

- Market Making bot: the service of quoting continuous passive trades prices to provide liquidity, and also be able to make some profits throughout this process.

- Arbitrage bot: takes advantage of small differences between markets. It is a trading activity that makes profits by exploiting the price differences of identical or similar financial instruments on different markets.

- Price mirroring bot: this bot uses liquidity and hedging possibilities from other markets to make the markets in a profitable way.

- Triangular Arbitrage bot: using this bot a trader could use the opportunity of exploiting the arbitrage opportunity from three different FX currencies or Cryptocurrencies.

- Basket Orders bot: with this bot, it is possible to execute trades on multiple coins at the same time with the possibility to hedge against other coins.

- VWAP bot: using this bot a trader can achieve the best price with large order by splitting it into multiple smaller ones throughout the trading day.

- Smart Order Routing bot: with this bot, the trader can find the best price for your order on all crypto exchanges and execute it.

In case you would need help from professional software developers to help you build proprietary trading bots and integrate it with API of Deribit or other crypto exchanges, you can consult with our quant team.

Now Crypto. Lessons learned from over 10 years of developing trading software

By Michal Rozanski, CEO at Empirica.

Reading news about crypto we regularly see the big money inflow to new companies with a lot of potentially breakthrough ideas. But aside from the hype from the business side, there are sophisticated technical projects going on underneath.

And for new cryptocurrency and blockchain ideas to be successful, these projects have to end with the delivery of great software systems that scale and last. Because we have been building these kinds of systems for the financial markets for over 10 years we want to share a bit of our experience.

“Software is eating the world”. I believe these words by Marc Andreessen. And now the time has come for financial markets, as technology is transforming every corner of the financial sector. Algorithmic trading, which is our speciality, is a great example. Other examples include lending, payments, personal finance, crowdfunding, consumer banking and retail investments. Every part of the finance industry is experiencing rapid changes triggered by companies that propose new services with heavy use of software.

If crypto relies on software, and there is so much money flowing into crypto projects, what should be looked for when making a trading software project for cryptocurrency markets? Our trading software development projects for the capital and crypto markets as well as building our own algorithmic trading platform has taught us a lot. Now we want to share our lessons learned from these projects.

- The process – be agile.

Agile methodology is the essence of how software projects should be made. Short iterations. Frequent deliveries. Fast and constant feedback from users. Having a working product from early iterations, gives you the best understanding of where you are now, and where you should go.

It doesn’t matter if you outsource the team or build everything in-house; if your team is local or remote. Agile methodologies like Scrum or Kanban will help you build better software, lower the overall risk of the project and will help you show the business value sooner.

- The team – hire the best.

A few words about productivity in software industry. The citation is from my favourite article by Robert Smallshire ‘Predictive Models of Development Teams and the Systems They Build’ : ‘… we know that on a small 10 000 line code base, the least productive developer will produce about 2000 lines of debugged and working code in a year, the most productive developer will produce about 29 000 lines of code in a year, and the typical (or average) developer will produce about 3200 lines of code in a year. Notice that the distribution is highly skewed toward the low productivity end, and the multiple between the typical and most productive developers corresponds to the fabled 10x programmer.’.

I don’t care what people say about lines of code as a metric of productivity. That’s only used here for illustration.

The skills of the people may not be that important when you are building relatively simple portals with some basic backend functionality. Or mobile apps. But if your business relies on sophisticated software for financial transactions processing, then the technical skills of those who build it make all the difference.

And this is the answer to the unasked question why we in Empirica are hiring only best developers.

We the tech founders tend to forget how important it is to have not only best developers but also the best specialists in the area which we want to market our product. If you are building an algo trading platform, software for market makers or trading bots, you need quants. If you are building banking omnichannel system, you need bankers. Besides, especially in B2B world, you need someone who will speak to your customers in their language. Otherwise, your sales will suck.

And finally, unless you hire a subcontractor experienced in your industry, your developers will not understand the nuances of your area of finance.

- The product – outsource or build in-house?

If you are seriously considering building a new team in-house, please read the points about performance and quality, and ask yourself the question – ‘Can I hire people who are able to build systems on required performance and stability levels?’. And these auxiliary questions – can you hire developers who really understand multithreading? Are you able to really check their abilities, hire them, and keep them with you? If yes, then you have a chance. If not, better go outsource.

And when deciding on outsourcing – do not outsource just to any IT company hoping they will take care. Find a company that makes systems similar to what you intend to build. Similar not only from a technical side but also from a business side.

Can outsourcing be made remotely without an unnecessary threat to the project? It depends on a few variables, but yes. Firstly, the skills mentioned above are crucial; not the place where people sleep. Secondly, there are many tools to help you make remote work as smooth as local work. Slack, trello, github, daily standups on Skype. Use it. Thirdly, find a team with proven experience in remote agile projects. And finally – the product owner will be the most important position for you to cover internally.

And one remark about a hidden cost of in-house development, inseparably related to the IT industry – staff turnover costs. Depending on the source of research, turnover rates for software developers are estimated at 25% to even 38%. That means that when constructing your in-house team, every fourth or even every third developer will not be with you in a year from now. Finding a good developer – takes months. Teaching a new developer and getting up to speed – another few months. When deciding on outsourcing, you are also outsourcing the cost and stress of staff turnover.

- System’s performance.

For many crypto projects, especially those related with trading, system’s performance is crucial. Not for all, but when it is important, it is really important. If you are building a lending portal, performance isn’t as crucial. Your customers are happy if they get a loan in a few days or weeks, so it doesn’t matter if their application is processed in 2 seconds or in 2 minutes. If you are building an algo trading operations or bitcoin payments processing service, you measure time in milliseconds at best, but maybe even in nanoseconds. And then systems performance becomes a key input to the product map.

95% of developers don’t know how to program with performance in mind, because 95% of software projects don’t require these skills. Skills of thinking where bytes of memory go, when they will be cleaned up, which structure is more efficient for this kind of operation on this type of object. Or the nightmare of IT students – multithreading. I can count on my hands as to how many people I know who truly understand this topic.

- Stability, quality and level of service.

Trading understood as an exchange of value is all about the trust. And software in crypto usually processes financial transactions in someway.

Technology may change. Access channels may change. You may not have the word ‘bank’ in your company name, but you must have its level of service. No one in the world would allow someone to play with their money. Allowing the risk of technical failure may put you out of business. You don’t want to spare on technology. In the crypto sapce there is no room for error.

You don’t achieve quality by putting 3 testers behind each developer. You achieve quality with processes of product development. And that’s what the next point is about.

- The DevOps

The core idea behind DevOps is that the team is responsible for all the processes behind the development and continuous integration of the product. And it’s clear that agile processes and good development practices need frequent integrations. Non-functional requirements (stability and performance) need a lot of testing. All of this is an extra burden, requiring frequent builds and a lot of deployments on development and test machines. On top of that there are many functional requirements that need to be fulfilled and once built, kept tested and running.

On many larger projects the team is split into developers, testers, release managers and system administrators working in separate rooms. From a process perspective this is an unnecessary overhead. The good news is that this is more the bank’s way of doing business, rarely the fintech way. This separation of roles creates an artificial border when functionalities are complete from the developers’ point of view and when they are really done – tested, integrated, released, stable, ready for production. By putting all responsibilities in the hands of the project team you can achieve similar reliability and availability, with a faster time to the market. The team also communicates better and can focus its energy on the core business, rather than administration and firefighting.

There is a lot of savings in time and cost in automation. And there are a lot of things that can be automated. Our DevOps processes have matured with our product, and now they are our most precious assets.

- The technology.

The range of technologies applied for crypto software projects can be as wide as for any other industry. What technology makes best fit for the project depends, well, on the project. Some projects are really simple such as mobile or web application without complicated backend logic behind the system. So here technology will not be a challenge. Generally speaking, crypto projects can be some of the most challenging projects in the world. Here technologies applied can be the difference between success and failure. Need to process 10K transaction per second with a mean latency under 1/10th ms. You will need a proven technology, probably need to resign from standard application servers, and write a lot of stuff from scratch, to control the latency on every level of critical path.

Mobile, web, desktop? This is more of a business decision than technical. Some say the desktop is dead. Not in trading. If you sit whole day in front of the computer and you need to refer to more than one monitor, forget the mobile or web. As for your iPhone? This can be used as an additional channel, when you go to a lunch, to briefly check if the situation is under control.

- The Culture.

After all these points up till now, you have a talented team, working as a well-oiled mechanism with agile processes, who know what to do and how to do it. Now you need to keep the spirits high through the next months or years of the project.

And it takes more than a cool office, table tennis, Xbox consoles or Friday parties to build the right culture. Culture is about shared values. Culture is about a common story. With our fintech products or services we are often going against big institutions. We are often trying to disrupt the way their business used to work. We are small and want to change the world, going to war with the big and the powerful. Doesn’t it look to you like another variation of David and Goliath story? Don’t smile, this is one of the most effective stories. It unifies people and makes them go in the same direction with the strong feeling of purpose, a mission. This is something many startups in other non fintech branches can’t offer. If you are building the 10th online grocery store in your city, what can you tell your people about the mission?

Final words

Crypto software projects are usually technologically challenging. But that is just a risk that needs to be properly addressed with the right people and processes or with the right outsourcing partner. You shouldn’t outsource the responsibility of taking care of your customers or finding the right market fit for your product. But technology is something you can usually outsource and even expect significant added value after finding the right technology partner.

At Empirica we have taken part in many challenging crypto projects, so learn our lessons, learn from others, learn your own and share it. This cycle of learning, doing and sharing will help the crypto community build great systems that change the rules of the game in the financial world!

Algorithmic crypto trading: market specifics and strategy development

By Marek Koza, Product Owner of Empirica’s Algo Trading Platform

Among trading professionals, interest in cryptocurrency trading is steadily growing. At Empirica, we see it by an increasing number of requests from trading companies, commonly associated with traditional markets, seeking algorithmic solutions for cryptocurrency trading or developing trading software with us from scratch. However, new crypto markets suffer from old and well-known problems. In this article, I try to indicate the main differences between traditional and crypto markets and take a closer look at a few algorithmic strategies (known as trading bots on crypto markets) that are currently effective in the crypto space. Differences between crypto and traditional markets constitute an exciting and deep subject in itself, which is evolving quickly as

the pace of change in crypto is also quite fast. But here I only want to focus on algorithmic trading perspectives.

LEGISLATION

First, there is a lack of regulations in terms of algorithmic usage. Creating DMA algorithms on traditional markets requires a great deal of additional work to meet reporting and measure standards as well as limitations rules provided by regulators (e.g., EU MiFIDII or US RegAT). In most countries, crypto exchanges have yet to be covered by legal restrictions. Nevertheless, exchanges provide their own internal rules and technical limitations, which, in a significant way, restrict the possibility of algorithmic use, especially in the HFT field. This is crucial for market-making activities, which now require separate deals with trading venues.

DERIVATIVES

As for market-making, we should notice an almost non-existent derivatives market in the crypto world. Even if a few exchanges offer futures and options, they only apply to a few of the most popular cryptocurrencies. Combining it with highly limited margin trading possibilities and none of the index derivatives (contracts that reflect market pricing), we see that many hedging strategies are almost impossible to execute and may only exist as a form of spot arbitrage.

As for market-making, we should notice an almost non-existent derivatives market in the cryptoworld. Even if a few exchanges offer futures and options, they only apply to a few popular cryptocurrencies. Combining it with highly limited margin trading possibilities and none of the index derivatives (contracts that reflect market pricing), we see that many hedging strategies are almost impossible to execute and may only exist as a form of spot arbitrage.

DECENTRALIZATION

The above-mentioned facts are slightly compensated for by the biggest advantage of blockchain currencies – fast and direct transfers around the world without banks intermediation. With cryptoexchange APIs mostly allowing automation of withdrawal requests, it opens up new possibilities for algorithmic asset allocation by much smaller firms than the biggest investment banks. This is important due to two things. Firstly, there is still no one-stop market brokerage solution we know from traditional markets. Secondly, cryptocurrency trading is distributed among many exchanges around the world. It could therefore be tricky for liquidity seekers and heavy volume execution. It implies there is still much to do for execution algorithms, such as smart order routing.

CONNECTIVITY

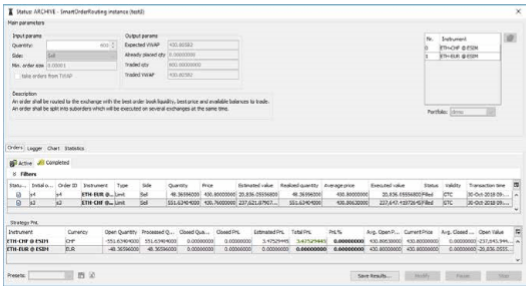

A smart order routing strategy GUI

Another difference is direct market access for algorithmic trading. While on traditional markets, DMA is costly, cryptocurrency exchange systems provide open APIs for all their customers that may be used without upfront prerequisites. Although adopted protocols are usually easy to implement, they are often too simplistic. They do not usually offer advanced order types. Besides, the order life-cycle status following is cumbersome and trading protocols differ among exchanges since each one requires its own implementation logic. That makes a costly technical difference compared to traditional markets with common standards, including FIX protocol.

MARKET DATA

Fast, precise and up-to-date data are crucial from an algorithmic trading perspective. When a trader develops algorithms for cryptocurrencies, she should be aware of a few differences. APIs provided by crypto exchanges give easy access to time & sales or level II market data for everyone for free. Unfortunately, data protocols used in the crypto space are unreliable, and trading venue systems often introduce glitches and disconnections. Moreover, not every exchange supports automatic updates and an algorithm has to issue a request every time it needs to check on the state of a market, which is difficult to reconcile with algorithmic strategies.

The APIs of most exchanges allow downloading of historical time & sale data, which is important in the algorithmic developing process. However, historical level II data are not offered by exchanges. We should also notice that despite being immature, the systems of crypto trading venues are evolving and becoming more and more professional. This forces trading systems to follow and adapt to these changes, which adds big costs to systems’ maintenance. In the following sections I overview a few trading algorithms that are currently popular among crypto algo traders because of the differences between traditional and crypto markets listed above.

SMART ORDER ROUTING

Liquidity is, and probably will remain, one of the biggest challenges for cryptocurrency trading. Trading on bitcoin and Ethereum, and all other altcoins with smaller market capitalization, is split among over 200 different exchanges. Executing a larger volume of assets often requires seeking liquidity in more than one trading venue. To achieve that, cryptocurrency traders may apply smart order routing strategies. These follow limit order books for the same instrument from different exchanges and aggregate them internally. When an investment decision is made, the strategy splits the order among exchanges that offer the best prices for the instrument. A well-designed strategy will also manage partially filled orders left in the order book in case some volume disappears before the order has arrived at the market. This strategy could be combined with other execution strategies such as TWAP or VWAP.

Empirica algorithmic trading platform front-end app (TradePad) for crypto-markets.

ARBITRAGE

The days when simple cross-exchange arbitrage was profitable with manual execution are over. Nowadays, price differences among exchanges for the most actively trading crypto assets are much smaller than a year ago and transactional and transfer costs (especially for fiat) still remain at a high level. Trading professionals are now focused on using more sophisticated arbitrage algorithms such as maker-taker or triangular arbitrage. The former works by quoting a buy order on one exchange, based on VWAP, for a particular amount of volume from another exchange (the same instrument) decreased by expected fees and return. A strategy is actively moving quoted order and if the passive gets executed, it sends a closing order to the other exchange. As the arbitrage is looking for bid-bid and ask-ask difference and maker fees are often lower, this type of arbitrage strategy is more cost-effective.

Triangular arbitrage may be executed on a single exchange because it looks for differences among three currency pairs that are connected to each other. To illustrate, let us use this strategy with BTCUSD, ETHUSD, and ETHBTC pairs. This strategy keeps following order books of these three instruments. The goal is to find the inefficient quoting and execute trades on three instruments simultaneously. To understand this process, we should notice that the ratio between BTCUSD and ETHBTC should reflect the ETHUSD market rate. Contrary to some FX crosses, all cryptocurrency pairs are priced independently. This creates numerous possibilities for using triangular arbitrage in the crypto space.

MARKET MAKING

Market making should be considered more as a type of business than as just a strategy. The main task of a market maker is to provide liquidity to markets by maintaining bid and ask orders to allow other market participants to trade any time they need. Since narrow spreads and adequate prices are among the biggest

factors of the exchange’s attractiveness, market making services are in high demand. On the one hand, crypto exchanges have special offers for liquidity providers, but on the other hand, they require from new coins issuers a market maker before they start listing an altcoin.

These agreements are usually one source of market maker income. Another one is a spread – a difference between a buy and a sell price provided to the other traders. The activity of a market maker is related to some risks. One of them is inventory imbalance – if a market maker buys much more than sells or sells much more than buys, she stays with an open long or short position and takes portfolio risk, especially in volatile crypto markets. This situation may happen in markets with a strong bias or when market maker is quoting wrong or delayed prices, which arbitrageurs will immediately exploit. To avoid such situations, market makers apply algorithmic solutions such as different types of fair price calculations, trade-outs, hedging, trend, and order-flow predictions, etc. Technology and math used in market making algorithms are exciting subjects for future articles.

SUMMARY

Fast-developing crypto markets are attracting many participants, including more and more trading professionals from traditional markets. However, the crypto space has its own specificity, such as high decentralization, maturing technology, and market structure. Compared to other markets, these differences make some strategies more useful and profitable than others. Arbitrage – even simple cross-exchange is still very popular. Market making services are in high demand. Midsized and large orders involve execution algorithms like smart order routing. To embrace the fast-changing crypto environment, one needs algorithmic trading systems with an open architecture that evolves alongside the market.

Follow us: